Often, we fall prey to not being able to see the forest because of the trees. The details overwhelm us and we miss the proverbial big picture. When it comes to the compliance of your credit calculations, I’m afraid these days the opposite may be taking place.

The nuances and parameters driving the calculations that create credit disclosures reside at such an esoteric, granular level that a long list of “900 lb. Gorillas” is currently over- crowding the room — disparate impact, fair lending, ATR, QM, UDAAP, HMDA data — none of which are focused on the integrity of how you calculate your traditional disclosures.

The consumer credit mathematics is often overlooked and, yes, taken for granted that it’s “just math” and influenced by the “we just need to find someone with an advanced mathematics degree” mindset.

But if you have ever spent much time trying to unravel your institution’s settings, parameters, interest accrual methods, rounding options etc., you know the consumer credit math is its own animal when compared to mainstream, everyday arithmetic.

With the expansion of regulatory requirements, it is paramount that all facets of a lender’s operation “cross foot and balance,” so to speak. We are calling that process “alignment.”

Alignment means the same methods are used throughout the life of the transaction. The narrative description in the lending agreement states that the lender will compute and accrue charges according to certain rules and parameters. The disclosure numbers populating the agreement are the product of employing those rules and parameters. The back-end servicing calculations actually collect the charge in the exact same manner. It all matches.

Sounds simple, right?

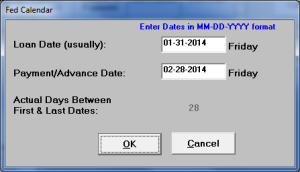

You would be surprised how often we see lending documents state that “charges will be computed on a 365-day year” in the promise to pay section, yet the numbers populating the form are generic, periodic, 30/360, HP 12C type calculations.

Those generic calculations are much simpler to program and compute and, most likely, have been embedded in the loan origination system for decades. We’ve got an incongruity right off the bat and we haven’t even gotten to the servicing calculations yet.

There is a train of thought that “it all comes out in the wash” with the interest-bearing, a.k.a. “simple interest”, transactions that dominate today’s credit market. “The consumer isn’t going to make all of their payments exactly on due dates anyway, so what’s the big deal about the regular payment?”

Well, besides the advent of debit/e-check/ACH payment proliferation rendering the previous adage practically unserviceable, there is the battle to define, determine, and evade the newly created CFPB two-headed specter of “deceptive” and “abusive”.

What better defense than all phases of your operation accurately and consistently portraying the contractual obligation between the lender and the borrower?

It might be worthwhile to step out of the dense compliance forest for just a moment and take a close look at the tree that houses your system calculation engine.